Introduction

The finance teams of retail businesses run on tight margins and deadlines as behind every product on the shelf is a vendor invoice and in a mid to large retail operation, that would mean hundreds of SKU-level invoices arriving daily from dozens of suppliers. For CFOs, the question would be no longer whether to automate accounts payable but how quickly would the business will not be able to afford. The manual AP processes in retail would not just slow down the finance team and make supplier relationships weak and create audit gaps that would compound quietly.

The Problem: Volume, Variance and Velocity

Retail accounts receivable automation would be uniquely complex as compared to service firms where invoices would be few and large, retail operations would deal with high-frequency, low-value transactions which would be tied down to specific SKUs, purchase orders and goods-received notes (GRNs). This would create three compounding challenges for CFOs.

Volume without structure-A single retail chain would process 500-2000 invoices every week across categories, seasons and locations. Every invoice would need to be matched against a PO and a GRN which would be a three-way match before payment would be approved. If this process is done manually, it would take days per batch and would require a specific headcount.

Variance at the line-item level- Retailers would frequently invoice at a slightly different rate than the PO which would be due to trade promotions, seasonal pricing changes or quantity adjustments. Identifying these discrepancies would manually mean line-by-line review which most accounts payable teams would simply don’t have time to do consistently.

Velocity pressure from both sides. The suppliers would want to be paid on time to maintain credit terms while the finance teams will want to hold cash as long as possible to protect liquidity lawfully. A manual account payable would not be able to optimise both at the same time as it just processes invoices in the order they arrive, leaving early-payment discounts uncaptured and DPO management to do the guesswork.

The result of the above problems would be late payment penalties, strained vendor relationships, missed discount windows and a finance team spending 60-70% of their time on data entry instead of financial oversight.

The Solution: AI-Powered AP Automation Built for Retail

The modern accounts payable automation is designed to handle exactly this kind of structured complexity at scale.

Touchless invoice processing would use intelligent OCR and machine learning to extract invoice data automatically, map it to the correct PO and GRN and validate quantities and prices at the SKU level. Invoices that would match perfectly would be approved and queued for payment without human intervention. The only genuine exceptions would be price mismatches, missing GRNs, duplicate line items which can be escalated to the accounts payable team.

Three-way matching at line-item granularity would mean the system that would check each SKU row individually, not just the invoice total. This would catch vendor overcharges that would otherwise pass through undetected.

Dynamic payment scheduling will allow the finance function to prioritise invoices based on discount capture opportunity, vendor credit terms and current cash position thus turning accounts receivable automation from a passive processing function into an active working capital tool.

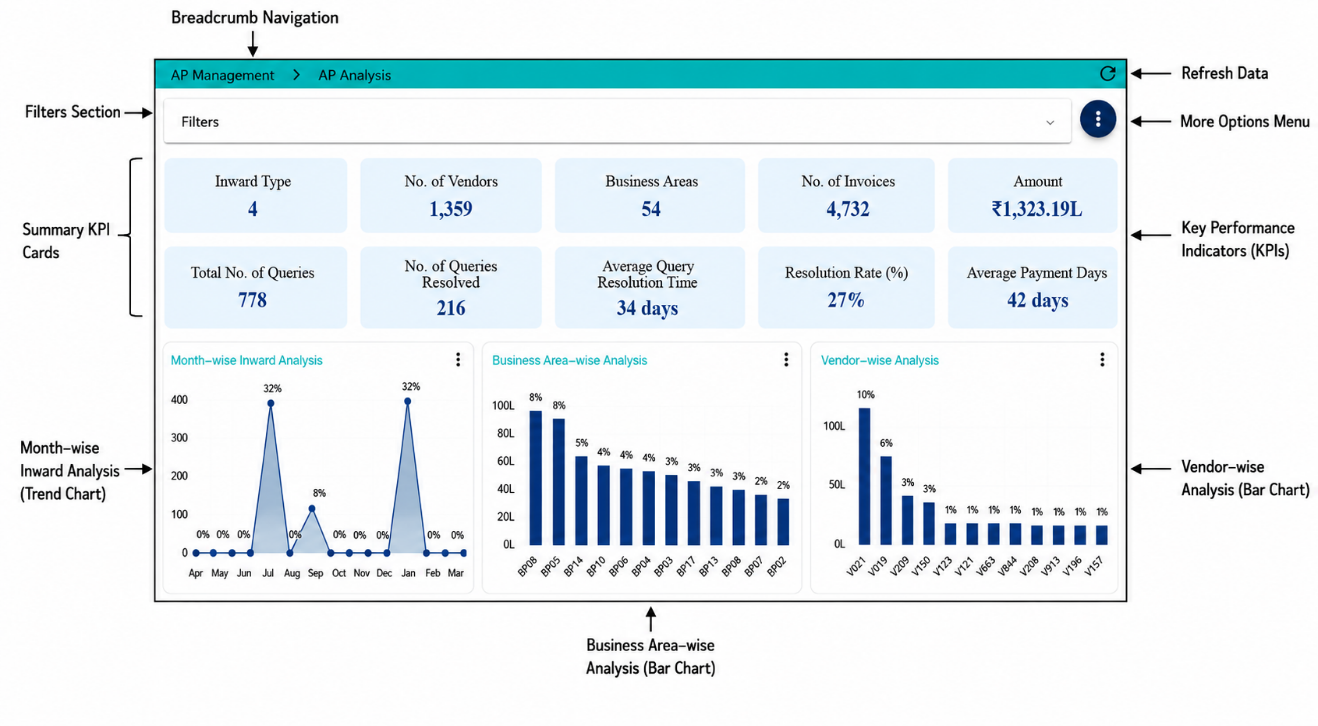

Real-time dashboards would give CFOs a live view of payables ageing, vendor-wise outstanding and cash outflow forecasts by replacing the weekly Excel update with continuous visibility.

For CFOS in retail managing multi-location operations this would mean accounts payable would scale with the business rather than requiring proportional headcount growth.

Conclusion

Retail accounts payable automation would not just be a back-office efficiency project but a growth driver for CFOs who want a better cash control, stronger vendor relationships and a finance team which would be focused on decisions rather than data entry. An AI-powered platform that would handle SKU-level matching, exception routing and payment optimisation would be able to reduce invoice processing costs by up to 75% while cutting cycle time significantly. For retail finance leaders, the real question would be not just whether automation would pay for itself but how much it’s costing to wait.

Frequently Asked Questions

Q1. How does AP automation handle SKU-level discrepancies in retail invoices?

AI-based accounts payable platform would perform three-way matching at the line-item level by comparing each SKUs invoiced quantity and price against the purchase order and goods received note. When a variance is detected (even a small one), the invoice would be flagged for human review rather than approved automatically. This would prevent overcharges from slipping through in high-volume retail environments where manual line-by-line review is impractical.

Q2. Will AP automation work with our existing ERP or accounting software?

Yes, modern accounts receivable automation automation solution can integrate with major ERP and accounting systems via API and pre-built connectors. The automation layer would sit on top of your existing systems in read-only or write-back mode thus meaning there would be no disruption to your core financial data or processes during implementation.

Q3. How long does it typically take to see ROI from retail AP automation?

Most retail finance teams would see measurable ROI within 60-90 days after going live. The primary savings would come from three areas: reduced manual processing costs (from Rs 800-1200 per invoice under 200), elimination of late payment penalties and capture of early-payment vendor discounts that would be previously missed. For mid-market retailers processing 1000+ invoices per month, the payback period would be typically under six months.